Main Story

The rules of flying post COVID-19

The first shoots of airline regrowth are sprouting in the Asia-Pacific, but so too are the gnarly weeds of post pandemic debt. Associate editor and chief correspondent, Tom Ballantyne, reports on the staggering cost of the industry’s battle to avoid destruction from COVID-19.

June 1st 2020

As an increasing number of Asia-Pacific airlines announce re-launches of domestic and international flights it is becoming clear the region where the coronavirus pandemic originated is leading the recovery charge. Read More » It engenders optimism, said International Air Transport Association (IATA) director general and CEO, Alexandre de Juniac, last month. “It shows a phased restart plan is the most reasonable approach to recovery. It’s a restart plan by phase, starting with domestic, then regional then intercontinental. It’s not surprising Asia, where the pandemic started a few weeks before other regions, is paving the way for the others,” he said.

It is a view endorsed by Association of Asia Pacific Airlines (AAPA) director general, Subhas Menon. “Whilst severe travel restrictions continue to limit the early restart of aviation activity, there are some encouraging signs in the market,” he said.

|

|

|

|

“A number of airlines are restoring domestic flights. A small number of international flights are still being operated with plans to operate additional services as border restrictions are progressively relaxed.”

At the same time, Menon said patchy, uncoordinated measures across countries, including various screening protocols and often onerous quarantine requirements, are deterring passengers from flying and slowing the process of restarting aviation.

“Countries in the Asia-Pacific were the first to encounter COVID-19 and are the first to witness some stabilization and degree of control over the spread of the disease. Hopefully, the region can lead the much-needed recovery in air travel,” he said.

The region’s latest traffic statistics, for April, were released by the AAPA at press time. They confirmed the dismal traffic numbers being reported by individual Asia-Pacific airlines for the period.

International passenger numbers had plunged 98.8% year-on-year, to 368,000, compared with 31.9 million passengers in the same month last year. Average international passenger load factor slumped to a historical low of 28.0% for the month. Available seat capacity declined 94.6% in the reported 30 days over April 2019.

At the same time, there were signs the worst may be over. Several airlines have announced resumption of some services, both domestic and international, for June and July. Singapore’s Changi airport and Hong Kong International Airport have opened their doors to transit traffic for the first time since the crisis began. Domestic flying, already resumed significantly in China, has restarted in India and is increasing in Korea and Japan.

But a return to significant long-haul flying remains years away, said IATA. Global airline RPKs (revenue passenger kilometres) in 2021 could be 32% to 41% lower than in 2019. By 2025 they could still be down 10%.

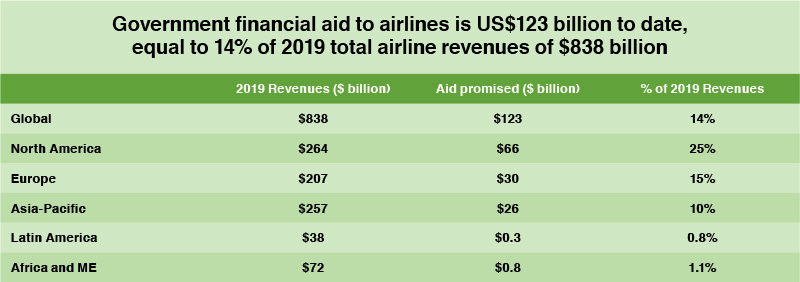

IATA chief economist, Brian Pearce, said in late May government aid to airlines in various forms, from loans to wage subsidies and cash injections, was $123 billion, far short of the $800 billion plus carriers earned in 2019.

Several Asia-Pacific nations have failed local airlines in COVID-19 crisis

His analysis laid bare that some Asia-Pacific governments had failed to provide sufficient relief to their airlines even though the industry is a critical contributor to their economies.

U.S. carriers had received government aid as high as 25% of 2019 revenues. European airlines were given 15% of their 2019 revenues. Asia-Pacific carriers received 10%. Airlines in India, Thailand, the Philippines, Malaysia, Vietnam and Indonesia were virtually shunned by their governments. Australian airlines received 1.8% in government aid as a percentage of their 2019 ticket revenues. Japanese operators on the other hand, were allocated 22.1% and Korean carriers 11.6%, respectively, of their revenue last year. The best supported airline industry was in Singapore, where the airline group received 84.2% of its 2019 revenues in government aid.

“Many governments have stepped up with financial aid packages that provide a bridge over this most difficult situation, including cash to avoid bankruptcies,” said de Juniac. “Where governments have not responded fast enough or with limited funds, we have seen bankruptcies. Examples include Australia, Italy, Thailand, Turkey and the UK. Connectivity will be important to the recovery.

“Meaningful financial aid to airlines makes economic sense. It will ensure they are ready to provide job supporting connectivity as economies re-open.

“For those governments that have not yet acted, the message is helping airlines raise equity levels with a focus on grants and subsidies will place them in a stronger position for the recovery.

“A tough future is ahead of us. Post-pandemic control measures will make operations more costly. Fixed costs will have to be spread over fewer travelers. Investments will be needed to meet our environmental targets. On top of all that, airlines will need to repay massively increased debts arising from the financial relief. After surviving the crisis, recovering to financial health will be the next challenge for many airlines,” de Juniac said.

|

Korean carriers extend restart to regional destinations

Boosted by government support, South Korean carriers are leading the return to international and domestic flying. Hanjin-controlled Jin Air is commencing flights from Incheon Seoul to Bangkok, Hanoi, Taipei, Narita and Osaka this month, two months after the LCC suspended the routes when passenger traffic collapsed. Jin Air said the decision was made after considering demand from Korean residents living abroad, students and business travelers and increased air cargo volume to the destinations.

Korean Air (KAL) said it was resuming some services to preemptively react to an increase in passenger numbers as the pandemic spread slows. It will restart 13 of the 110 international routes it had operated pre-COVID-19. Next month, up to 32 international routes connecting Seoul to Washington D.C., Seattle, Amsterdam, Frankfurt, Kuala Lumpur, Yangon, Hanoi and Singapore will be available.

Rival Asiana Airlines will operate 27 of its 73 international routes from June, aimed mainly to recover routes to China including Beijing, Shanghai, Nanjing and Qingdao.

The major Gulf carriers, with their heavy reliance on transit traffic, are rapidly restoring their global networks. At the turn of the month, Emirates announced more flights will become available between Dubai and Amsterdam, Bahrain, Brisbane, Chicago, Copenhagen, Dublin, Frankfurt, Kuala Lumpur, Jakarta, London Heathrow, Madrid, Manila, Melbourne, Milan, Paris, Perth, Singapore and Vienna from June 15. Frequencies to Hong Kong are to be increased three a week. Travelers from the Asia-Pacific can transit through the Emirate to Europe and The Americas and bookings to Copenhagen, Manchester, Seoul and Taipei soon will be opened. Travellers must meet all immigration entry requirements of their destination countries.

Qatar Airways said the gradual rebuilding of its network is continuing with restoration of flights from Doha to Bangkok. Barcelona, Islamabad, Karachi, Lahore, Peshawar, Singapore and Vienna and services to Berlin, Dar es Salaam, New York, Tunis and Venice to soon follow. Flights from Doha to Dublin, Milan and Rome are to be increased or returned to daily.

Singapore and Hong Kong have been accepting transit passengers from June 1, but their feed is limited by the fact Australian and New Zealand carriers only are operating domestic networks and have not restarted international flights.

| Global industry debt to hit US$550 billion this year IATA’s analysis showed the airline industry’s global debt could rise to $550 billion by year-end, a $120 billion, or 28% increase, over January 2020. The $67 billion in new debt was made up of government loans ($50 billion), deferred taxes ($5 billion) and loan guarantees ($12 billion). Approximately $52 billion of the support funding came from commercial sources, including commercial loans ($23 billion), capital market debt ($18 billion), debt from new operating leases ($5 billion) and access to existing credit facilities ($6 billion). “More than half of the relief provided by governments creates new liabilities. Less than 10% will add to airline equity. It changes the financial picture of the industry completely. Paying off the debt owed to governments and private lenders will mean the crisis will last a lot longer than the time it takes for passenger demand to recover,” said de Juniac. |